Why Overpricing Your House Can Cost You

If you’re trying to sell your house, you may be looking at this spring season as the sweet spot – and you’re not wrong. We’re still in a seller’s market because there are so few homes for sale right now. And historically, this is the time of year when more buyers move, and competition ticks up. That makes this an exciting time to put up that for sale sign.

But while conditions are great for sellers like you, you’ll still want to be strategic when it comes time to set your asking price. That’s because pricing your house too high may actually cost you in the long run.

The Downside of Overpricing Your House

The asking price for your house sends a message to potential buyers. From the moment they see your listing, the price and the photos are what’s going to make the biggest first impression. And, if it’s priced too high, you may turn people away. As an article from U.S. News Real Estate says:

“Even in a hot market where there are more buyers than houses available for sale, buyers aren't going to pay attention to a home with an inflated asking price.”

That’s because no homebuyer wants to pay more than they have to, especially not today. Many are already feeling the pinch on their budget due to ongoing home price appreciation and today’s mortgage rates. And if they think your house is overpriced, they may write it off without even stepping foot in the front door, or simply won’t make an offer if they think it’s priced too high.

If that happens, it’s going to take longer to sell. And ideally you don’t want to have to think about doing a price drop to try to re-ignite interest in your house. Why? Some buyers will see the price cut as a red flag and wonder why the price was reduced, or they’ll think something is wrong with the house the longer it sits. As an article from Forbes explains:

“It’s not only the price of an overpriced home that turns buyers off. There’s also another negative component that kicks in. . . . if your listing just sits there and accumulates days on the market, it will not be a good look. . . . buyers won’t necessarily ask anyone what’s wrong with the home. They’ll just assume that something is indeed wrong, and will skip over the property and view more recent listings.”

Your Agent’s Role in Setting the Right Price

Instead, pricing it at or just below current market value from the start is a much better strategy. So how do you find that ideal asking price? You lean on the pros. Only an agent has the expertise needed to research and figure out the current market value for your home.

They’ll factor in the condition of your house, any upgrades you’ve made, and what other houses like yours are selling for in your area. And they’ll use all of that information to find that target number. The right price will bring in more buyers and make it more likely you’ll see multiple offers too. Plus, when homes are priced right, they still tend to sell quickly.

Bottom Line

Even though you want to bring in top dollar when you sell, setting the asking price too high may deter buyers and slow down the sales process.

Let’s connect to find the right price for your house, so we can maximize your profit and still draw in eager buyers willing to make competitive offers.

What To Save for When Buying a Home

🏠 Knowing what to budget for when buying a home may feel intimidating — but it doesn’t have to be. By understanding the costs you may encounter upfront, you can take control of the process.…. Read more….

Read More

Home Staging FAQ: What You Need To Know

🏠 You may have heard that staging your home properly can make a big difference when you sell your house, but what exactly is home staging, and is it really worth your time and effort?…. Read more….

Read More

The Top 2 Reasons To Look at Newly Built Homes

🏠 When planning a move, a newly built home might not be the first thing that comes to mind. But with more brand-new homes on the market and builders focusing on smaller, more affordable options, this type of home may…. Read more….

Read More

Timo Rivetti has been serving his clients with a highly individualized service tailored to specific needs and requirements since 1998. Unparalleled knowledge and expertise in the region is invaluable when it comes to buying and selling real estate. Hiring an agent who knows the area inside out makes all the difference in a competitive market. Timo and his team of experienced professionals work with each and every client to find and secure the perfect property at the best price, with all of the required amenities in the right neighborhood. When it’s time to make a move, call Timo.

What My Clients Have To Say

WHY NAVIGATE REAL ESTATE

If you live here already, you know how blessed we are. If you're considering living or investing here, you've probably experienced some of the area's extraordinary possibilities: country settings and small-town communities; enthralling agricultural beauty, and true farm to fork lifestyle, If Northern California is your real estate destination, you've arrived at the right spot. Whether you're looking to buy your first home - or to sell an estate - expect nothing less from us than a Meritage blend of real estate expertise, professional service, creativity, and a passion for achieving your goals.

Arts Alive April 18th with Suzanne Young

This month, artist Suzanne Young will feature her work on Thursday April 18th, from 5pm to 8pm. Stop by for a glass of wine and enjoy our new downtown space at 140 Second Street, Suite 108. Suzanne has been busy creating new art this spring and is excited to share it. Check out her diverse portfolio at suzanneyoung.art

ARTS ALIVE connects and promotes

Petaluma's vibrant arts community.

Join us on the third Thursday of each month in

a citywide celebration of art and artists.

Arts Alive’s mission is to connect, promote, and celebrate Petaluma’s vibrant arts community. It is a city-wide eclectic art experience occurring monthly

on the third Thursday from 5pm-8pm. The public will experience live music, dance, theater, improv, storytelling, art demonstrations, poetry, book launches, photography, dance parties, multimedia exhibits, film, and more. Arts Alive is currently taking place at various host locations throughout Petaluma and

expanding rapidly as the vision takes off. Attendance is free. Some venues may suggest reservations.

Timo Rivetti, Rivetti Real Estate and Navigate Real Estate are proud to participate in the Arts Alive "Pop-Up lounge in our office. Last month we featured artist and ceramicist Mary Fassbinder. We were delighted to visit with so many of our client family and friends during the inaugural event.

Timo Rivetti has been serving his clients with a highly individualized service tailored to specific needs and requirements since 1998. Unparalleled knowledge and expertise in the region is invaluable when it comes to buying and selling real estate. Hiring an agent who knows the area inside out makes all the difference in a competitive market. Timo and his team of experienced professionals work with each and every client to find and secure the perfect property at the best price, with all of the required amenities in the right neighborhood. When it’s time to make a move, call Timo.

What My Clients Have To Say

WHY NAVIGATE REAL ESTATE

If you live here already, you know how blessed we are. If you're considering living or investing here, you've probably experienced some of the area's extraordinary possibilities: country settings and small-town communities; enthralling agricultural beauty, and true farm to fork lifestyle, If Northern California is your real estate destination, you've arrived at the right spot. Whether you're looking to buy your first home - or to sell an estate - expect nothing less from us than a Meritage blend of real estate expertise, professional service, creativity, and a passion for achieving your goals.

CELEBRATING 15 YEARS WITH REALTOR ASSOCIATE AND EXECUTIVE ASSISTANT RENEE’ WATERS

In this modern age of rapid change, it’s extraordinary to be celebrating our 15th anniversary as a team, with Realtor Associate and Executive Assistant Renee’ Waters.

“From day one, she has been our steadying

force. We could not have navigated the roller

coaster of real estate without her consistency,

dedication, skilled professionalism, humor and good spirits,” says Timo. “Renee’ has been steadfast in helping countless homeowners ready their houses for the market over the years and steered them through the complexity of paperwork that makes a successful sale.”

Renee’ shares a common dedication to family life and to our Sonoma County community with Timo and Frances. We all hold firm to the belief that work/life balance is key to an ongoing successful team. Thank you, Renee’ for so many wonderful years working together. Drop in and say hello to Renee’ and Timo at the NAVIGATE RE office in Theatre Square next time you are downtown.

Timo Rivetti has been serving his clients with a highly individualized service tailored to specific needs and requirements since 1998. Unparalleled knowledge and expertise in the region is invaluable when it comes to buying and selling real estate. Hiring an agent who knows the area inside out makes all the difference in a competitive market. Timo and his team of experienced professionals work with each and every client to find and secure the perfect property at the best price, with all of the required amenities in the right neighborhood. When it’s time to make a move, call Timo.

What My Clients Have To Say

WHY NAVIGATE REAL ESTATE

If you live here already, you know how blessed we are. If you're considering living or investing here, you've probably experienced some of the area's extraordinary possibilities: country settings and small-town communities; enthralling agricultural beauty, and true farm to fork lifestyle, If Northern California is your real estate destination, you've arrived at the right spot. Whether you're looking to buy your first home - or to sell an estate - expect nothing less from us than a Meritage blend of real estate expertise, professional service, creativity, and a passion for achieving your goals.

SPRING CLEANING IN ONE MONTH

Week One: We know you want to, but let’s be real... Don’t attempt to spring clean your entire house all at once. Break it down to different zones per week. Professional organizers suggest kick starting a spring clean in high-traffic areas first. Start with the Family Room to round up all the clutter that has built up over the winter: old newspapers, magazines, books, blankets, and candles. Anything that doesn’t belong in the room should be put back where it came from, donated, or ditched! Next up is the Dining Area. Seasonal décor and tableware from the holidays should be done and dusted by April. Go through that pile of mail and then on to other common dumping grounds. Remove things that have gathered dust and don’t serve a purpose on all surfaces.

Week Two: Kitchen confidential! It’s time to confess, the clutter is real. Sort through the refrigerator, pantry, cabinets and drawers. Discard expired food, update cleaning supplies, donate extra dishes and cookware you never use. It’s time for some fresh, new kitchen towels and containers!

Week Three: Bedroom refresh. It’s time to reorganize the closet, sort through clothing that needs donating, repairing or dry cleaning. Look through the linen closet to remove any items that have seen better days. Maybe it’s time for new sheets? Bedside tables, drawers and dressers will benefit from a clean out too! Then don’t forget the laundry room.

Week Four: Bathrooms are notorious for collecting junk. Sort through medicine cabinets, drawers and countertops. Freshen towels and rugs if needed. Last, but not least, don’t forget the garage. A seasonal sort out is essential after the winter. Donate bags of unwanted items gathered from around the house this month. Sweep and prepare for summer.

Timo Rivetti has been serving his clients with a highly individualized service tailored to specific needs and requirements since 1998. Unparalleled knowledge and expertise in the region is invaluable when it comes to buying and selling real estate. Hiring an agent who knows the area inside out makes all the difference in a competitive market. Timo and his team of experienced professionals work with each and every client to find and secure the perfect property at the best price, with all of the required amenities in the right neighborhood. When it’s time to make a move, call Timo.

What My Clients Have To Say

WHY NAVIGATE REAL ESTATE

If you live here already, you know how blessed we are. If you're considering living or investing here, you've probably experienced some of the area's extraordinary possibilities: country settings and small-town communities; enthralling agricultural beauty, and true farm to fork lifestyle, If Northern California is your real estate destination, you've arrived at the right spot. Whether you're looking to buy your first home - or to sell an estate - expect nothing less from us than a Meritage blend of real estate expertise, professional service, creativity, and a passion for achieving your goals.

ADDRESSING PETALUMA’S HOUSING NEEDS

Petaluma Argus Courier recently reported that the City of Petaluma has achieved more than 20% of its housing allocation requirements in the first year of a state- mandated eight-year housing cycle that calls for 1,910 new housing units through 2031. The housing element is a requirement under the city’s General Plan. It facilitates production of new housing for various income levels, households and family types in order to promote fair housing.

A housing specialist for the city told the council in March that the remaining 1,515 housing units will be spread over four different income categories of very low, low, moderate and above average income. Already, the city has provided 40% of the above moderate category housing, so we should expect to see more affordable units as the focus going forward. And of the 389 affordable units that are already in the pipeline, 119 permanent supportive units will help to provide a pathway from shelter to longer term housing solutions.

Accessory Dwelling Units (ADUs) are being identified as a key strategy to additional affordable housing. Petaluma City Council approved new housing design standards for streamlining qualifying residential projects, back in February, including tree coverage minimums, no vinyl exteriors and 150 ft maximum building facades. “There’s a lot of push-back on both sides as to the construction of new units in Petaluma,” says Timo. “The fact is, the city’s general plan anticipated significantly more growth in population than we have seen. In order to house the folk who do live here, their adult children and the people who work in our schools and services, we must expect development in infill areas.”

One of the projects being eyed for future cycles is the 143-unit Oyster Cove project on East D Street by the river. Expect to see a variety of residential unit sizes in three to four-story condo buildings. This project will comply with the city’s housing requirements, with 15% of units reserved for low and moderate-income households. This project is awaiting building permits. “Petaluma continues to juggle supply and demand,” says Timo. “For such a desirable place to live, there are more buyers than there are sellers, especially for mid-market properties.

If you are thinking of selling, now is a great time to talk strategy. I expect there to be robust interest in homes in the Petaluma area this Spring and Summer.” Call me at 707-477-8396

Timo Rivetti has been serving his clients with a highly individualized service tailored to specific needs and requirements since 1998. Unparalleled knowledge and expertise in the region is invaluable when it comes to buying and selling real estate. Hiring an agent who knows the area inside out makes all the difference in a competitive market. Timo and his team of experienced professionals work with each and every client to find and secure the perfect property at the best price, with all of the required amenities in the right neighborhood. When it’s time to make a move, call Timo.

What My Clients Have To Say

WHY NAVIGATE REAL ESTATE

If you live here already, you know how blessed we are. If you're considering living or investing here, you've probably experienced some of the area's extraordinary possibilities: country settings and small-town communities; enthralling agricultural beauty, and true farm to fork lifestyle, If Northern California is your real estate destination, you've arrived at the right spot. Whether you're looking to buy your first home - or to sell an estate - expect nothing less from us than a Meritage blend of real estate expertise, professional service, creativity, and a passion for achieving your goals.

Does It Make Sense To Buy a Home Right Now?

Thinking about buying a home? If so, you're probably wondering: should I buy now or wait? Nobody can make that decision for you, but here's some information that can help you decide.

What’s Next for Home Prices?

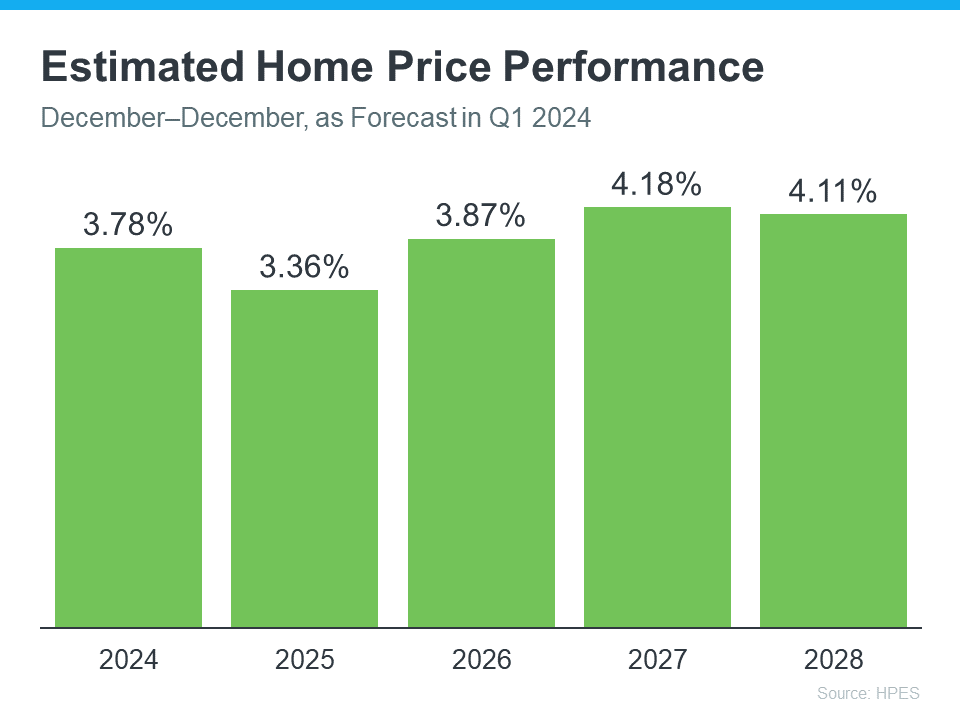

Each quarter, Fannie Mae and Pulsenomics publish the results of the Home Price Expectations Survey (HPES). It asks more than 100 experts—economists, real estate professionals, and investment and market strategists—what they think will happen with home prices.

In the latest survey, those experts say home prices are going to keep going up for the next five years (see graph below):

Here’s what all the green on this chart should tell you. They’re not expecting any price declines. Instead, they’re saying we’ll see a 3-4% rise each year.

And even though home prices aren’t expected to climb by as much in 2025 as they are 2024, keep in mind these increases can really add up over time. It works like this. If these experts are right and your home's value goes up by 3.78% this year, it's set to grow another 3.36% next year. And another 3.87% the year after that.

What Does This Mean for You?

Knowing that prices are forecasted to keep going up should make you feel good about buying a home. That’s because it means your home is an asset that’s projected to grow in value in the years ahead.

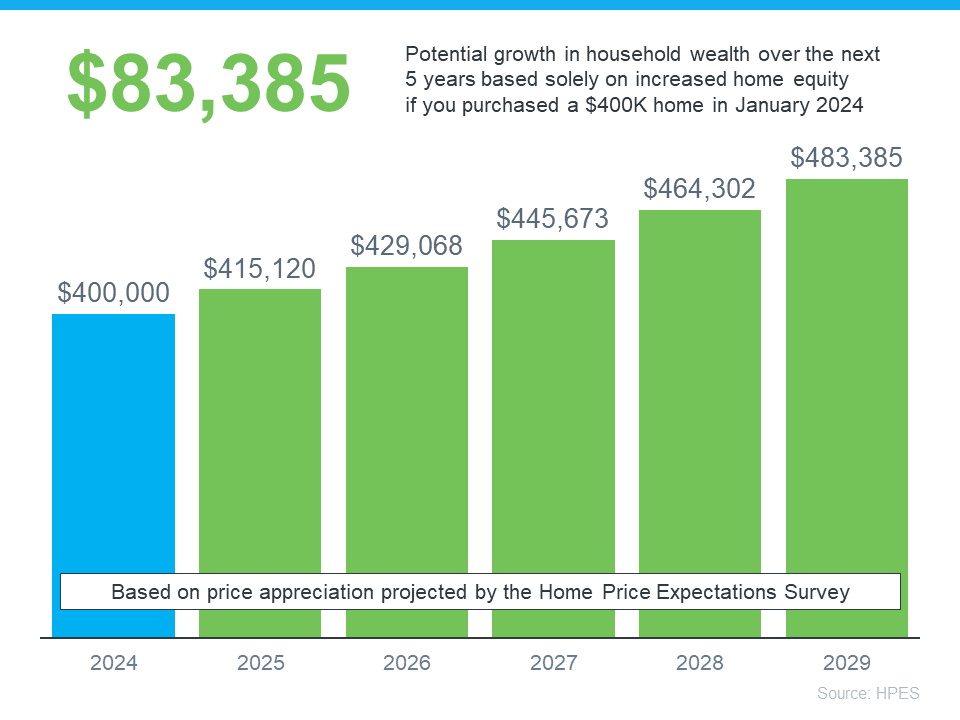

If you’re not convinced yet, maybe these numbers will get your attention. They show how a typical home’s value could change over the next few years using expert projections from the HPES. Check out the graph below:

In this example, imagine you bought a home for $400,000 at the start of this year. Based on these projections, you could end up gaining over $83,000 in household wealth over the next five years as your home grows in value.

Of course, you could also wait – but if you do, buying a home is just going to end up costing you more.

Bottom Line

If you're thinking it's time to get your own place, and you’re ready and able to do so, buying now might make sense. Your home is expected to keep getting more valuable as prices go up. Let’s team up to start looking for your next home today.

2-2 1/2 Grandview Ave, Petaluma, CA 94952

FOR SALE 2-2 1/2 Grandview Ave Petaluma, CA $835,000 Beds3 Baths2 Living Area1,472 sq ft Year Built1932 MLS# 326051766 Petaluma, CA 2-2 1/2 Grandview Ave 🏢 3 Beds 🛀 2 Baths 📌 1,472 sq ft 📅 Built 1932 $835,000 × ← → Property Highlights ●MLS# 326051766●3 Bedrooms●2 Bathrooms●1,472 sq ft Living Area●0.1205 acres Lot Size●Built […]

Read More

450 Amber Way, Petaluma, CA 94952

MLS# 326039716 5 bedrooms 3 bathrooms Approximately 3,000 sq. ft. 0.3152-acre private lot Contemporary architectural style Desirable West Petaluma location Perched at hilltop setting Sweeping hillside views Views of hills, mountains, valley Updated and remodeled condition Split-level floorplan Cathedral ceiling detail Natural light throughout Beautifully updated kitchen Stone kitchen counters Breakfast area Pantry closet Built-in […]

Read More

7 Lavender Ter, Petaluma, CA 94952

MLS# Available Upon Request 5 bedrooms 3 full bathrooms Approx. 2,750 sq ft Approx. 11,192 sq ft lot Built in 2000 West Petaluma location Roseview neighborhood Two-story home Remodeled kitchen High ceilings Wide plank pine floors Light-filled interiors Spacious living areas Flexible floor plan Fireplace 11 total rooms Private backyard Established landscaping Room to garden […]

Read More888 Petaluma Blvd S, Petaluma, CA 94952

MLS #325080809 4 bedrooms total 3 full bathrooms 2,626 square feet Built in 2015 Two-story design Cordelia neighborhood Garibaldi Ranch community Leased solar panels Two Tesla Powerwalls EV charging outlet Granite kitchen counters Large center island Open living and dining Fresh interior paint Central heat and air Main floor bedroom Upstairs loft space Laundry on […]

Read More

Timo Rivetti has been serving his clients with a highly individualized service tailored to specific needs and requirements since 1998. Unparalleled knowledge and expertise in the region is invaluable when it comes to buying and selling real estate. Hiring an agent who knows the area inside out makes all the difference in a competitive market. Timo and his team of experienced professionals work with each and every client to find and secure the perfect property at the best price, with all of the required amenities in the right neighborhood. When it’s time to make a move, call Timo.

What My Clients Have To Say

WHY NAVIGATE REAL ESTATE

If you live here already, you know how blessed we are. If you're considering living or investing here, you've probably experienced some of the area's extraordinary possibilities: country settings and small-town communities; enthralling agricultural beauty, and true farm to fork lifestyle, If Northern California is your real estate destination, you've arrived at the right spot. Whether you're looking to buy your first home - or to sell an estate - expect nothing less from us than a Meritage blend of real estate expertise, professional service, creativity, and a passion for achieving your goals.

NAVIGATE REAL ESTATE PETALUMA LAUNCH PARTY A BIG SUCCESS!

Never mind the rain, more than 200 people turned out on a gloomy, wet Thursday afternoon and into the evening

for the official ribbon cutting and launch party of our newly revamped office space in Theatre Square.

The Navigate RE Team, along with agents from all over the North Bay and beyond gathered with Timo and Renee’s client family and friends including those of 13 newly signed agents in the updated Petaluma office for a fabulous launch party on Leap Year’s Day, February 29th.

“It was a fantastic gathering,” says Timo. “Thanks to the Navigate RE Team for a full-service bar, Sahar from La Dolce Vita Wine Bar for a steady flow of delicious appetizers and D.J Tanner Wyre with Paradise Found Records & Music in downtown Petaluma for spinning the discs, live.” (Visit La Dolce Vita at ldvwine.com and ParadiseFoundRecordsMusic.com for more information).

Petaluma Chamber of Commerce ribbon cutting attracted a large crowd, despite the rain. “It was so much fun and so warm and inviting inside that no one wanted to leave,” says Timo. If you missed it, there will be more frequent gatherings. “It’s a very inclusive spot,” says Timo. “I’m loving my new-look private office, come by and say hello if you see me in there!”

The office is located downtown at 140 Second Street #108 ... learn more about NavigateRE click here.

Timo Rivetti has been serving his clients with a highly individualized service tailored to specific needs and requirements since 1998. Unparalleled knowledge and expertise in the region is invaluable when it comes to buying and selling real estate. Hiring an agent who knows the area inside out makes all the difference in a competitive market. Timo and his team of experienced professionals work with each and every client to find and secure the perfect property at the best price, with all of the required amenities in the right neighborhood. When it’s time to make a move, call Timo.

What My Clients Have To Say

WHY NAVIGATE REAL ESTATE

If you live here already, you know how blessed we are. If you're considering living or investing here, you've probably experienced some of the area's extraordinary possibilities: country settings and small-town communities; enthralling agricultural beauty, and true farm to fork lifestyle, If Northern California is your real estate destination, you've arrived at the right spot. Whether you're looking to buy your first home - or to sell an estate - expect nothing less from us than a Meritage blend of real estate expertise, professional service, creativity, and a passion for achieving your goals.

ARTS ALIVE WITH ARTIST MARY FASSBINDER THURSDAY MARCH 21ST 5-8PM

Join us at our office on Thursday evening, March 21st for our first Arts Alive event, featuring Petaluma artist and ceramicist Mary Fassbinder. Refreshments served. Arts Alive connects and promotes Petaluma’s vibrant arts community every third Thursday at multiple events around town. Check out the schedule and locations for Arts Alive by clicking here.

“I’m delighted to feature local artists for my private office, art which can be viewed from Second Street,” says Timo. Currently featured are works by Gail Foulkes, Mary Fassbinder and Roberta Ahrens. “I’ve been collecting works by local artists for my home for a while,” says Timo. “It’s good to extend the practice to my office, downtown. Arts Alive is the perfect program to spotlight and showcase favorite artists in the area.”

Timo Rivetti has been serving his clients with a highly individualized service tailored to specific needs and requirements since 1998. Unparalleled knowledge and expertise in the region is invaluable when it comes to buying and selling real estate. Hiring an agent who knows the area inside out makes all the difference in a competitive market. Timo and his team of experienced professionals work with each and every client to find and secure the perfect property at the best price, with all of the required amenities in the right neighborhood. When it’s time to make a move, call Timo.

What My Clients Have To Say

WHY NAVIGATE REAL ESTATE

If you live here already, you know how blessed we are. If you're considering living or investing here, you've probably experienced some of the area's extraordinary possibilities: country settings and small-town communities; enthralling agricultural beauty, and true farm to fork lifestyle, If Northern California is your real estate destination, you've arrived at the right spot. Whether you're looking to buy your first home - or to sell an estate - expect nothing less from us than a Meritage blend of real estate expertise, professional service, creativity, and a passion for achieving your goals.

Timo Testimonial 5-Star Review

My wife and I had heard really positive things about Timo. We switched strategies with realtors and hired Timo after testimonials from his previous clients, all of whom praised his character, loyalty, and professionalism. We were immediately impressed with his authentic demeanor, as he came across with great enthusiasm and a sincere understanding of our journey.

He had the house on the market within three weeks. We didn’t have to stage it or move out, because he convinced us that these were unnecessary expenses and that the quality and location of our home was enough to stand on its own. He took into consideration our financial concerns, which we deeply appreciated. Here’s the magic: Timo had one open house and sold it to the first buyers who looked at it! Not only did he sell our house, but the people who were interested had a house in the exact area that we had been waiting a year to find. He immediately saw the potential for BOTH parties and was able to create a deal where the buyers would buy our house, and we could buy theirs! It was a storybook scenario for both parties, and Timo navigated us through all the uncharted territories of such an unusual real estate occurrence.

Timo is an outstanding real estate agent, and an extraordinary human being, with vital connections all over Sonoma County. He is at the pulse of everything that’s happening in real estate, and whether you are buying or selling, he will make sure that you reach your goals. Thank you Timo, for helping all of us start a new chapter in our lives. - Cambridge Seller

Timo Rivetti has been serving his clients with a highly individualized service tailored to specific needs and requirements since 1998. Unparalleled knowledge and expertise in the region is invaluable when it comes to buying and selling real estate. Hiring an agent who knows the area inside out makes all the difference in a competitive market. Timo and his team of experienced professionals work with each and every client to find and secure the perfect property at the best price, with all of the required amenities in the right neighborhood. When it’s time to make a move, call Timo.

What My Clients Have To Say

WHY NAVIGATE REAL ESTATE

If you live here already, you know how blessed we are. If you're considering living or investing here, you've probably experienced some of the area's extraordinary possibilities: country settings and small-town communities; enthralling agricultural beauty, and true farm to fork lifestyle, If Northern California is your real estate destination, you've arrived at the right spot. Whether you're looking to buy your first home - or to sell an estate - expect nothing less from us than a Meritage blend of real estate expertise, professional service, creativity, and a passion for achieving your goals.

MORE HOUSES ON THE MARKET IN PETALUMA THIS SPRING

The California housing market has shown its resilience this year, rebounding in January after a six month slump in the second half of 2023 when mortgage rates were at a high. According to real estate watch dogs, interest rates are expected to decline later this year, improving inventory throughout 2024.

California Association of Realtors has expressed optimism that the overall outlook for the housing market appears positive as pent-up demand translates into sales. There is an increase in active new listings in the Petaluma area. “While mortgage rate fluctuations may influence potential new buyers and sellers,” says Timo “the prospect of a softening in the economy and a downward trend in interest rates in the coming months is helping with increased inventory locally.” This should provide buyers with more financial flexibility. However, there is still likely to be a tight inventory in the Petaluma area as housing demand continues to exceed supply availability.

Forecasts predict a substantial 22.9 percent increase in existing, single-family home sales this year, compared to last year. “Homes are moving swiftly,” says Timo. “The current average home value in Petaluma is around $900,000 with homes on the West Side averaging around $1.1m.” Real estate remains more expensive in Bodega Bay, Healdsburg, Penngrove, Sebastopol and Sonoma, which makes Petaluma all the more appealing, price wise, for a desirable Sonoma County address.

“There’s been a downward trend in many Bay Area cities and counties,” says Timo, “Sonoma County on the other hand, retains its value for the money in real estate investments whether you are looking to buy a home for yourself or to rent out.”

Planning helps everyone be a step ahead in addition to having an agent that is highly aware of the local market. Timo is always available to discuss your goals, talk strategy, pivot as needed and work for you in this fast-changing market. Call him today at 707. 477. 8396

Timo Rivetti has been serving his clients with a highly individualized service tailored to specific needs and requirements since 1998. Unparalleled knowledge and expertise in the region is invaluable when it comes to buying and selling real estate. Hiring an agent who knows the area inside out makes all the difference in a competitive market. Timo and his team of experienced professionals work with each and every client to find and secure the perfect property at the best price, with all of the required amenities in the right neighborhood. When it’s time to make a move, call Timo.

What My Clients Have To Say

WHY NAVIGATE REAL ESTATE

If you live here already, you know how blessed we are. If you're considering living or investing here, you've probably experienced some of the area's extraordinary possibilities: country settings and small-town communities; enthralling agricultural beauty, and true farm to fork lifestyle, If Northern California is your real estate destination, you've arrived at the right spot. Whether you're looking to buy your first home - or to sell an estate - expect nothing less from us than a Meritage blend of real estate expertise, professional service, creativity, and a passion for achieving your goals.

Timo Rivetti

Broker Assoc. Managing Partner

NavigateRE

707.477.8396

timo@rivettiteam.com

DRE Lic# 01240796

DRE Lic# 02221115

Made with Love by navi © 2023